Have you thought about purchasing a rental home in the Las Vegas area? There are tons of investors sprouting up and making the rental homes in your area very completive. “When I first got started as an investor, I spent a lot of time trying to find these types of properties. I remember spending hours upon hours scanning my local MLS listings, desperately trying to find a deal that would make financial sense.” This quote was actually pulled directly out of the attached blog post. Most people are looking for a cheap home to buy as a rental, but don’t realize how much work goes into a rental home and making it livable for your future tenant! There are multiple steps when buying a rental property, and making your money worth the while! “If a deal doesn’t cash flow, don’t buy it. PERIOD. This is why it’s crucial for you to nail down your projections and get an accurate depiction of its profitability – because frankly, your “GO” or “NO GO” decision usually boils down to the answers you get after going through these motions.” That quote was also pulled from the article, and it truly stood out to me, because most people want to purchase a rental home but don’t factor in the mortgage vs how much they will be profiting off it. After you think about the financial part of the rental home, it is time to think about fixing and upgrading your rental home. “As with any real estate investment – buying rental properties takes a lot of homework. Rental properties don’t necessarily come with the glamour and huge paychecks that “flipping houses” is known for – but it is a proven method of building multiple streams of permanent income.” This quote that was also pulled out of the article explains that even though you most of the Rental Home process is about your research and everything that comes before purchasing, it is also about making the property a good investment, and making it so you get the best renter possible in it. In the article below, it tells you that in your first year of having a rental home that is the year you will more than likely have most of your problems because when you buy as is, you don’t know what you are truly getting. Don’t discouraged when your profit ratio is a little off the first year you own your property in the Las Vegas Area, because after that you should start seeing a more upward profit. “Again – this is not (nor will it ever be) a property that throws off massive cash flow, but for someone’s first experience with a rental property, it’s an ideal way to get started in the business.” Finishing this blog post off with another quote from the article because this is a strong statement saying your rental property most likely won’t make you tons and tons of money, but when it comes to starting a business in being an investor, a small rental property is the one to choose! Please read below for the attached article that gives you more information on this topic.

The Beginner’s Guide to Buying Rental Properties (A Case Study)

One of the primary objectives of my real estate business is to acquire income-producing rental properties that ROCK.

One of the primary objectives of my real estate business is to acquire income-producing rental properties that ROCK.

What makes a rental property “rock” you might ask?

It doesn’t necessarily need to pump millions into my bank account each month, and it doesn’t need to be a “no money down” deal either (although either of these things would certainly sweeten the pot).

To put it simply, a great rental property is one that makes every one of my invested dollars work hard. I want every penny to work overtime, producing as much revenue as possible while simultaneously paying off any debt associated with the property. When you buy properties with this goal in mind, there is basically no limit (mathematically speaking) to how far you can grow your net worth and personal income.

The Problem

When I first got started as an investor, I spent a lot of time trying to find these types of properties. I remember spending hours upon hours scanning my local MLS listings, desperately trying to find a deal that would make financial sense.

After running the numbers on dozens of properties, I was shocked at how difficult it was to find just one single property that would justify my investment.

At the time, it was 2005 and housing prices were through the roof – which made this a very difficult task (especially when I limited myself to ONLY the properties that were “listed”, with a realtor sign in the front yard). Needless to say, it was an extremely discouraging time in my journey.

I eventually realized I was dealing with two fundamental problems:

- I didn’t have an effective way to find motivated sellersand get them calling me. I was relying ONLY on unmotivated sellers who were holding out for top dollar. This was a losing strategy thatwasn’t going to cut it.

- I didn’t have an effective way to analyze properties or determine their potential profitability. I needed a basic, but highly reliable method so I could calculate exactly what I was getting into.

After a lot of research and learning, I was able to find some very effective ways to solve BOTH of these problems.

Both issues are equally important to deal with but for obvious reasons, problem #2 cannot be addressed until problem #1 has been dealt with. In other words, you can’t start working on your analysis until you have something to analyze. This may seem obvious, but it’s important to reiterate this so you can prioritize correctly and deal with first things first.

The Reason For This Case Study

The purpose of this guide is to show you exactly how I handle Problem #2 (above). If you haven’t figured out how to find motivated sellers yet, go and read this or this first and THEN come back to this case study.

I often find myself evaluating rental properties and consulting with other investors on how to find, evaluate and buy their own deals – so the purpose of this blog post is to explain exactly how I do this. This article is intended to provide a brief education, where I will show you the entire process that I go through when buying a rental property, which includes some of the following steps:

- First Contact with the Seller

- Quick Property Evaluation

- Running the Numbers

- Deal or No Deal?

- Offer and Acceptance

- Due Diligence

- Closing Process

- Wholesaling Overview

- What to Expect

- A Look Back (One Year Later)

- Final Thoughts

If you’re reading this, you may very well fall into one of these categories:

- You don’t know how to find a legitimate, profitable rental property.

- You understand the theory, but have never actually purchased a rental property before.

- You don’t understand how to analyze and evaluate a rental property the right way.

- You need a better understanding of how the entire process works, from start to finish.

- You don’t have a proper set of expectations about what a rental property should produce, and why investors buy them in the first place.

This blog post is intended to show you exactly what steps I go through, what my expectations are, and how I ensure my (or my client’s) return on investment is something they can be proud of.

I’m a pretty big fan of “on-the-job training”, so I figured the most practical way to show you this process would be to use a real life example I dealt with just a few short years ago.

First Contact with the Seller

In early December, I received a voicemail in response to one of my direct mail campaigns (I had usedTemplate #3 for this particular mail campaign, and I pulled my list using the same process I describe inthis blog post).

This mailing was actually sent out the previous summer (over a year earlier) – this guy had simply held onto my postcard and called me about 16 months later (gotta love the residual benefits of direct mail).

This was his first voicemail to me:(note: caller’s name and address have been removed from this recording for privacy)

Quick Property Evaluation

Once I got this message and learned the basic details about this property (i.e. – the owner’s full name and property address – which were edited out of the above audio clip), I went to work.

I was fortunate in some respects, because I was very familiar with this neighborhood. I had sold a similar house a few blocks away for $88,900 in late-2009 (by which time, the market had already taken a dive), so I had some perspective on what a house like this would legitimately be worth.

Before I called the prospect back, I went through my quick property research process and learned most of the pertinent details about this property. It was a single-family home with 2 bedrooms & 1 bathroom. According to the seller, it generated approximately $750 per month in rent. Using AgentPro247, I learned that the seller had purchased this property eight years earlier for $55,000 – which gave me some perspective on where he was coming from.

Armed with this basic information, I called the prospect back.

After roughly 4 minutes on the phone with the property owner, I asked him (point-blank) if he would sell his property for $30,000 – $40,000.

He replied very quickly with, “Yes, I would consider that.”

Later in the week, I called the seller back and told them that our offer would likely be for $25,000. He said that he would think about it.

A few days later (after hearing nothing from him), I called him again to see what he was thinking. He said that he was hoping for something more in the $30K – $40K like I initially stated (*kicking self*). I realized pretty quickly I should have suggested an even lower number to begin with. Setting his expectation in the $30K – $40K range right out of the gate probably wasn’t smart (it’s generally easier to start low and negotiate up, than to start high and negotiate down). Lesson learned.

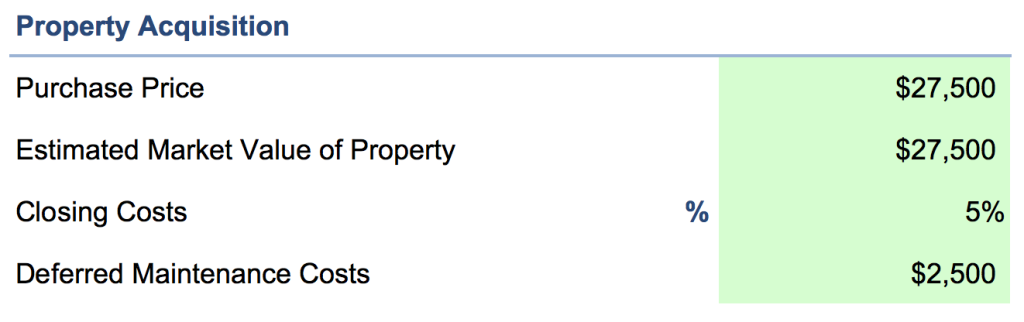

Eventually (after a few more discussions) we settled verbally on a price of $27,500 cash, with all closing costs paid by the buyer. In other words, the buyer (aka – me) would have to cough up another couple thousand dollars in order to close the deal (this includes things like title insurance, closing fees, property insurance, pro-rated property taxes, etc).

Show Me The Money

Now, most people don’t have $27,500 sitting in their checking account at any given time and at the time, I was no exception. Luckily, I knew some other investors who did.

I called one of my cash buyers and gave them a quick overview of the deal. They were very interested in finding out more. Like most people, they were stuck with Problem #1 (above). They had plenty of money to invest, but they didn’t know how to find good deals. These are excellent people to have on your buyers list because in their minds, any property at 70% or less of market value is an AMAZING deal that will get them very excited.

Luckily, I had mastered the art of finding cheap real estate in my area (FAR below 70% of market value) so when I told them about this property, I had their attention very quickly. I gave them a general overview of the property (“a 2 bedroom, 1 bathroom house on the southeast side of town, a 1.5 stall garage close to the local public school, etc.”). I also prepared a Rental Property Analysis to show them exactly what kind of ROI they could expect from this property as a rental unit (more details on that below).

After seeing my property prospectus report, my buyers said they were ready to gowith cash in hand, contingent on an acceptable home inspection and verification of all of all my assumptions.

Running The Numbers

One of the most important things you MUST do as you’re evaluating a new property are your projections.

“Projections” are basically just a series of highly informed guesses about how profitable a property may (or may not) be in the future. In order to figure this out, you’ll have to do a little bit of homework and develop a thorough understanding of what the income and expenses are likely to be from this property in the future.

It’s not difficult, but as with any real estate transaction, there are a number of things you need to pay close attention to. As you research a property and learn more about what you’re getting into – certain things matter greatly, and other things matter very little. My hope is that as we’re walking through this process, I can give you a good idea on what to look out for.

Many, MANY of the deals you’ll see on a regular basis won’t have positive cash flow (in fact, that’s almost exclusively what I saw in my first year as a real estate investor) – and there are a lot of things that can sabotage the profitability of a rental property. Things like:

- Paying too high a price for the property

- Excessive Property Taxes

- Excessive Interest Expense

- Insurance Costs

- Maintenance, Utilities and Upkeep

- Unforeseen Disasters

- Home Owner’s Association (HOA) Fees

If a deal doesn’t cash flow, don’t buy it. PERIOD. This is why it’s crucial for you to nail down your projections and get an accurate depiction of its profitability – because frankly, your “GO” or “NO GO” decision usually boils down to the answers you get after going through these motions.

Dealing With Imperfections

Are your projections going to be perfect? Not likely.We aren’t fortune tellers after all, so it’s impossible to know EXACTLY how things will pan out in the coming months and years.

Projections rarely come to fruition exactly as we plan, but when they’re done correctly, using realistic data and assumptions, they will almost always set you up with reasonably accurate expectations that won’t lead you astray. The numbers may turn out better or worse than you estimated, but they should at least come out somewhat similar to what you had originally predicted.

Challenge Your Assumptions

- So you think rent will be $750 per month? Says who?? Is this a reliable and unbiased source of information?

- You think the vacancy rate will be 10%? What makes you think so? Do you have any actual experience or market data to back this up?

- What kinds of maintenance and repairs will you have to take care of? How certain are you about what the costs will be?

- What if one or more of your assumptions turns out to be wrong? Does the property still perform to an acceptable standard?

In order to come up with your “best possible guess” at what the future is going to look like, you need to be armed with the right information. Your inputs will literally determine everything here, so remember the theory of “garbage in, garbage out”. If you start with bad information (or if you just guess at the numbers without really getting them from a credible source), you’re not going to have a very reliable number in the end.

The last thing we want is to invest our life savings into a property that loses money hand-over-fist.

![]() One of the best rental property evaluation tools I’ve ever found is called thePropertyREI Rental Property Calculator. It’s an easy-to-use excel spreadsheet that allows you to plug-in a few basic inputs, and (assuming your numbers are reasonably accurate) will show you some very clear results that will help you determine if/when you’re looking at a worthwhile real estate investment.

One of the best rental property evaluation tools I’ve ever found is called thePropertyREI Rental Property Calculator. It’s an easy-to-use excel spreadsheet that allows you to plug-in a few basic inputs, and (assuming your numbers are reasonably accurate) will show you some very clear results that will help you determine if/when you’re looking at a worthwhile real estate investment.

In the example below, I’ll show you how I used this calculator to go through the motions of plugging in the numbers so I could understand whether I was looking at a solid deal for an investor to pursue.

(Note: If you want to get a copy of this calculator for yourself, be sure to use Promo Code: RETIPSTER1at checkout for an instant 10% discount).

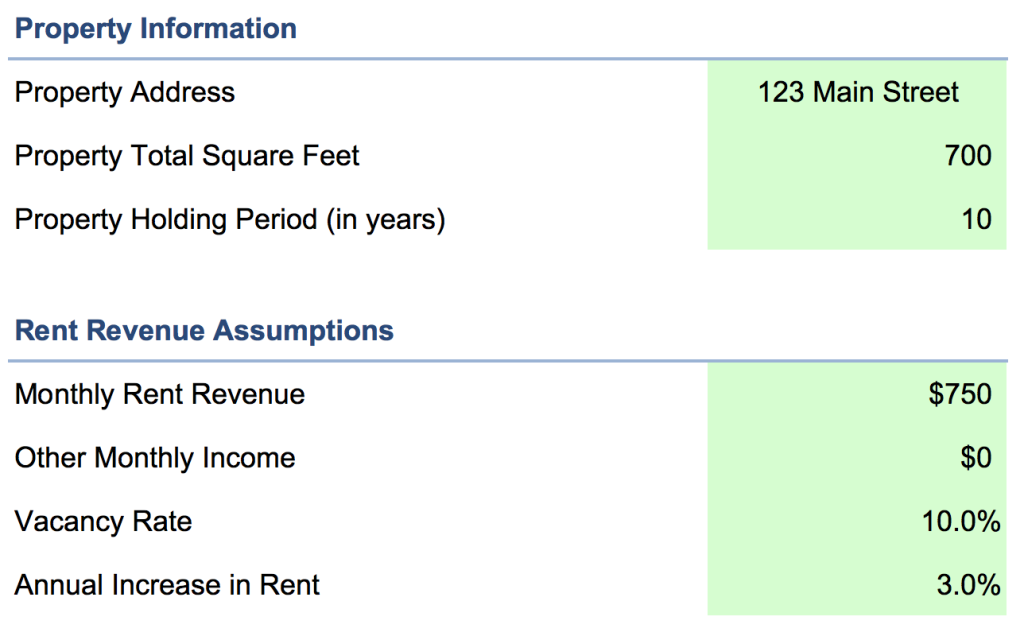

Step 1: Determine Your Rent Revenue

It all starts with having a solid understanding of the revenue your property is likely to generate every month. We’re talking gross income – before any/all expenses.

Now – in my first conversation with this seller, he told me that he was generating $750 per month in revenue from this house.

Can we trust him? There are a couple of ways to find out.

I started by asking him to send me Schedule E of his past two years of tax returns (a Schedule E is basically an income statement, showing the amount of revenue and expenses he reported to the IRS for this particular rental property). After reviewing his information, it turned out that he did make approximately $750/mo for the past two years.

I also ran the numbers on Rentometer – which gave me a quick look at what similar properties were renting for in the immediate vicinity. I found that $750 was a little on the high-end for the area, but not a completely unreasonable expectation.

I also gave my property manager a call to see if he thought this was a realistic expectation given the property and neighborhood. He expressed some hesitancy and mentioned that in his opinion, a more realistic number (in THIS neighborhood, for THIS kind of house) would be around $700.

In the end, since I had proof that $750 was attainable based on the seller’s tax returns (and since the property was being sold with the same tenant who had been paying that amount for the past 2 years), I decided to use this number in my calculation… but I would likely re-run the numbers again later with this $700 number, just to make sure the deal still produced adequate cash flow.

I also assumed the property would have no other sources of income (i.e. – no vending machines or coin laundry), a vacancy rate of 10% (i.e. – the property will be vacant and/or between tenants for 5 weeks out of the year… a pretty conservative estimate in this market) with the plan for increasing rent revenue each year by 3% on average.

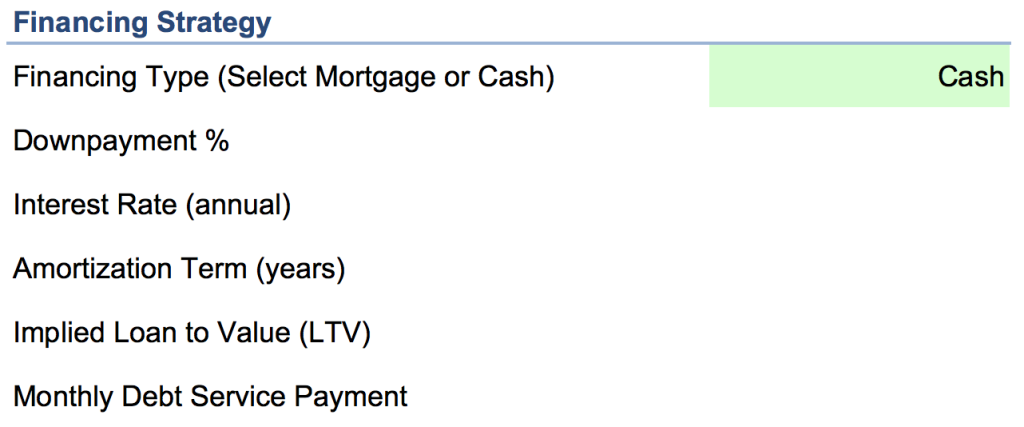

Step 2: Purchase Price and Financing

Depending on whether the property is being purchased with some form of financing, or whether it’s being purchased outright as an all cash deal – the financing picture will usually have a big effect on the outcome of your calculation.

In my example, the property was being purchased with cash – which greatly simplified this portion of the calculator.

Why was this property being purchased with cash instead of financing? A few reasons…

- The property was relatively inexpensive.

- The investor had the cash available.

- The investor was more concerned about generating more cash flow than about making their cash work harder for them (which we’ll get to in a minute).

For this deal, the closing costs came out to approximately $1,500 (which is actually closer to 5.5% – but not a huge variation from the 5% shown above) and the deferred maintenance costs we planned for were $2,500 (the furnace was in rough shape, so we assumed it would need to be replaced shortly after closing).

Step 3: Factoring in All Expenses

Understanding a property’s expenses can be a painful dose of reality.

These are the items that most sellers tend to downplay (or just fail to mention altogether)… but these numbers are CRUCIAL to understand.

These numbers are very real and will play a major role in the profitability (or lack thereof) of your rental property. You’ll have to do your homework in this section, and it’s important that you do this part of the process well because if you use the wrong numbers, you’ll only be fooling yourself and hurting your (or your buyer’s) future.

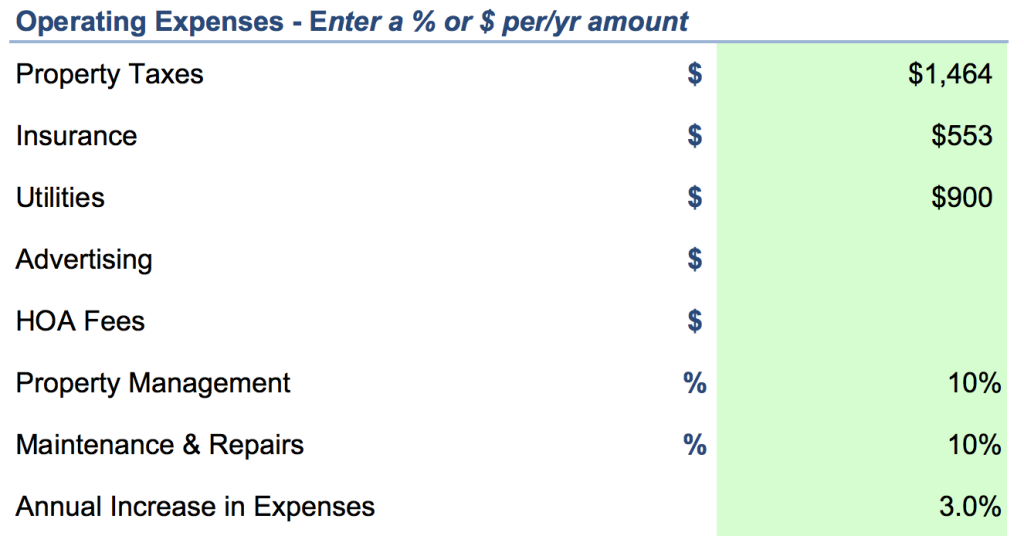

Property Taxes: Property taxes have always been a depressing subject for me. Why? Because regardless of whether you purchase a property with financing or you buy it free and clear, you will always have to pay property taxes. Since this expense is permanently attached to the property, it’s important that you find the correct number and factor it into your calculation. I found this number by checking the seller’s Schedule E and by checking the City Treasurer’s website for the total annual property taxes over the past two years. In the previous year, this property owner paid $1,464 in property taxes, so that was the number I used here.

Insurance: This one is pretty easy. You can call any property insurance agent (I recommend trying at least a couple to compare prices) and they will be more than happy to tell you what the annual cost will be. I called my property insurance agent and gave him the rundown, and he indicated an annual cost of$550 – $600 for this type of property. Given that the seller had paid $553 – I decided to use that number for this part of the calculation.

Utilities: For most residential rental properties in my town, utilities are set up in such a way that the landlord pays the water bill, but everything else is covered by the tenant. The utilities can be set up in a number of different ways, but whatever your arrangement is, you need to get a good idea on what this number will be on an annual basis.

In this situation, the seller also had the utilities arranged so that he paid ONLY the water bill. By looking at his Schedule E, I was able to see that he had paid an average of $900 per year for the past two years. Based on my own experience with my other rental properties in the area (and based on my property manager’s opinion), I knew this was a solid, legitimate number to work with.

Advertising: I use a great property management company for all of my rental properties (and I recommend all my buyers do the same). Most property managers will handle the placement and eviction of all tenants as part of their service, so we’ll get to this cost in the .

HOA Fees: This property is not part of a home owner’s association, so this step is easy. ZERO.

Property Management: Even if you’re not going to hire a property manager like I do (most property managers will charge around 10% of your gross rent revenue), you still need to pay yourself for your trouble. The fact is – somebody, in some way, will ALWAYS have to manage this property, so regardless of who is doing the job, this is a very real expense that ought to be accounted for.

Maintenance & Repairs: Another absolute must that you need to include in your expense column is a reserve for maintenance and repairs. I always plan to set aside at least 10% of my gross rent revenue to cover the issues that willcome up when my properties start falling apart (because sooner or later, it’s going to happen). Even if you have a year or two where no extraordinary expenses come up, you need to let these funds accumulate. All it takes is one roof replacement, or one pipe to burst in the basement and ALL of this money will be needed immediately – so let this money build up and don’t drain this account.

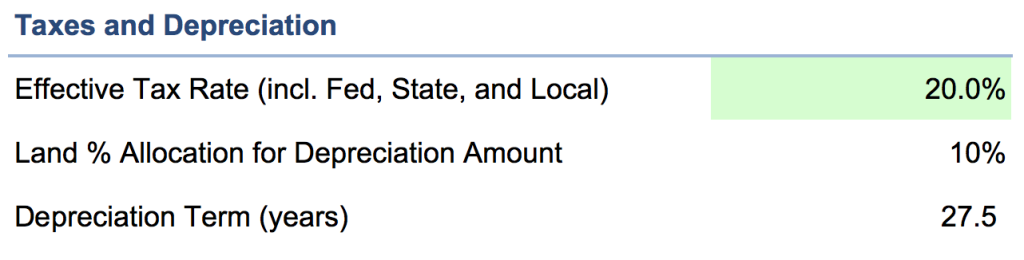

Step 4: Taxes and Depreciation

This next step is pretty simple. If you know what effective tax rate you’re working with (this will depend on the investor’s situation), you can plug it in and the calculator will factor this in to the final calculations of what your annual cash flow will be after taxes. I used 20% in my example.

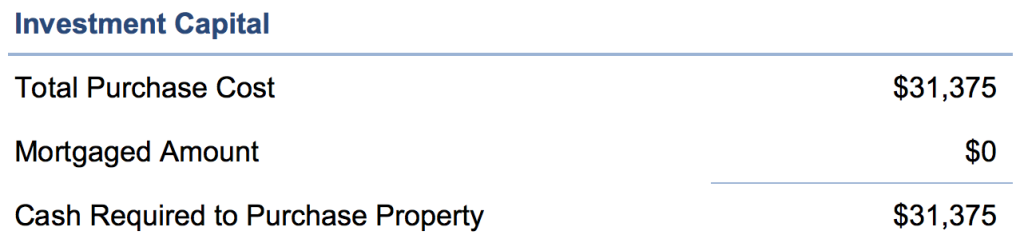

The calculator will also do a calculation to show what the TOTAL cost will be to purchase the property (in this case, it’s taking the purchase price of $27,500 + closing costs of $1,375 + deferred maintenance of $2,500 = $31,375 cash required to purchase property).

This simply shows us what the full acquisition cost will be, so there is no confusion about this deal is going to cost the investor.

Step 5: Executive Summary

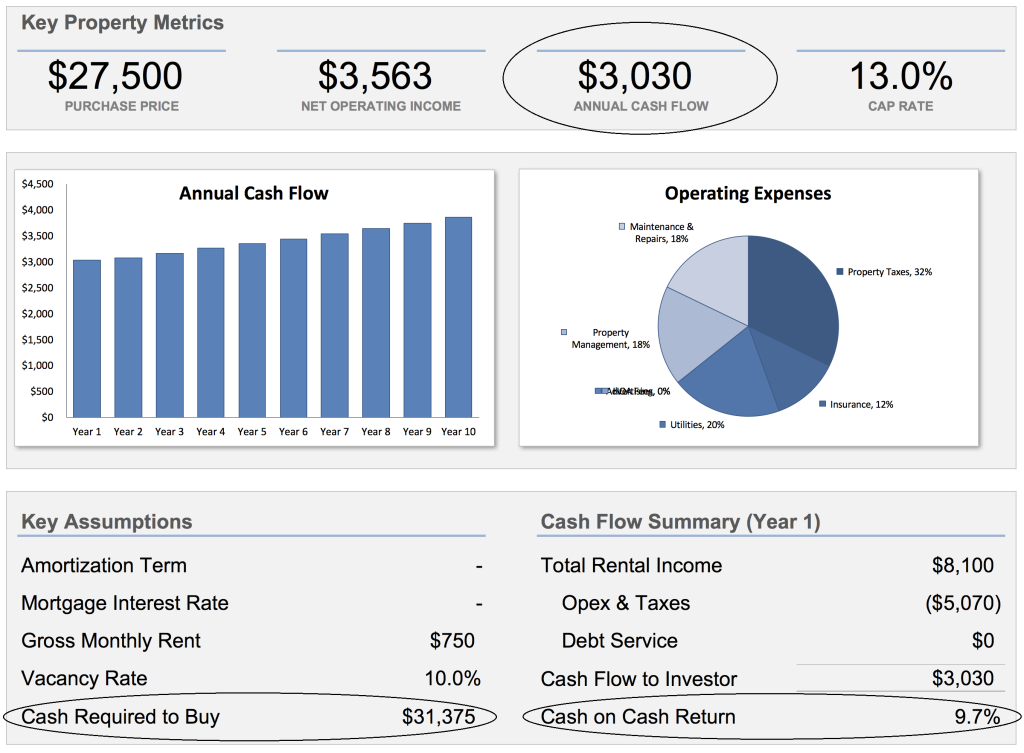

This is usually a very revealing part of the calculation process, because it gives us a good look at what kind of net revenue the property can actually be expected to generate (both before and after taxes).

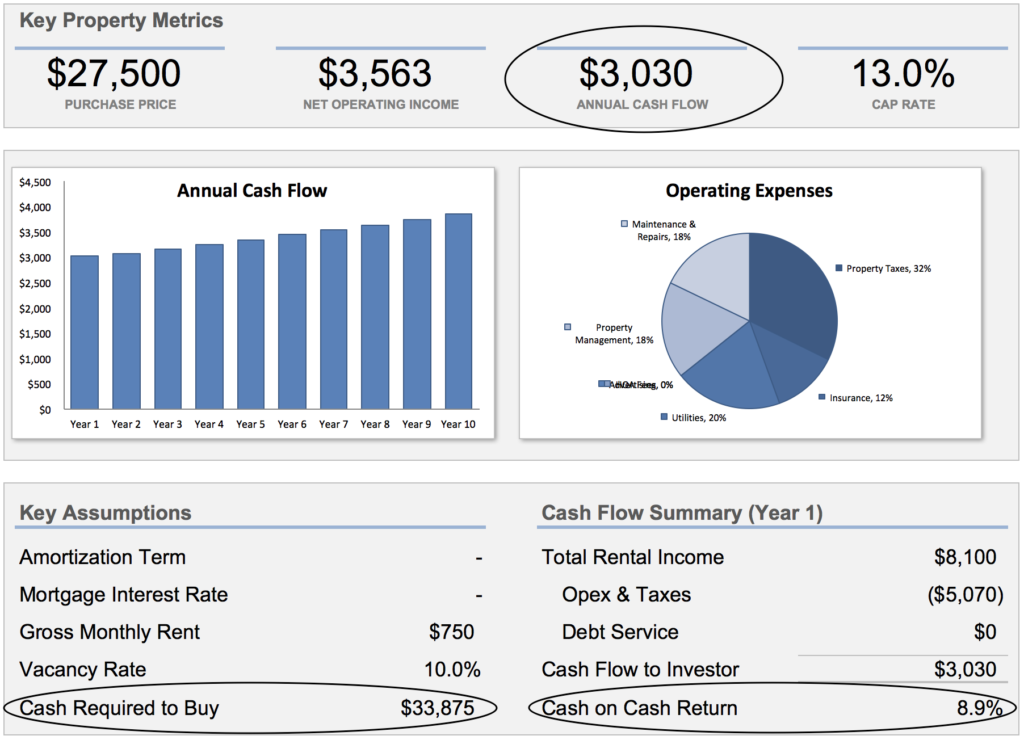

In the example below, the calculator is telling me that after all expenses, the investor would be adding another $3,563 to their annual income, and then the amount they would actually keep in their pocket (after their taxes are paid) would be $3,030. This is if the investor chooses to buy this property and pay all cash for it.

In a very real way, this information is your final, decision-making data, and depending on whether the property is being bought with cash or with financing – the end results can vary widely.

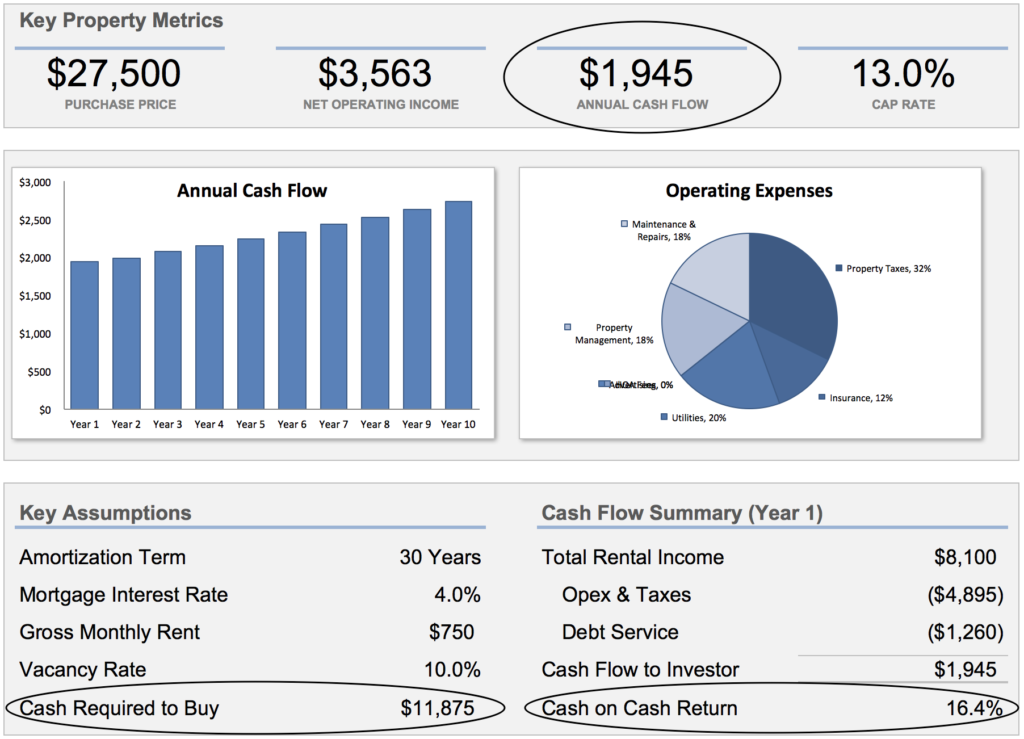

Some of the numbers I always watch very closely are the Annual Cash Flow, the Cash Required to Buy and the Cash on Cash Return.

For example, let’s go back to the Dashboard and change our financing strategy to buy this property with a mortgage. If we put down 20% and get a 30 year mortgage at an interest rate of 4.00% – we now have to add monthly loan payments of $105 into the mix.

What does this do to our numbers? Check out the differences…

When we use financing for a property like this, it comes with some tradeoffs. Let’s look at the pros and cons of using financing to buy this property.

Pros:

- If we utilize financing, this property (and the source of income that comes with it) will require significantly LESS cash to buy upfront.

- The Cash on Cash Return is over 2x higher when we use the power of “OPM” (Other People’s Money). In other words, every dollar we put into this property from our own pocket is going to work MUCH harder than if we had to cover the full purchase price without financing.

Cons:

- Since we’ll have to make monthly loan payments for the next 30 years, the annual cash flow is going to see a significant negative impact. Although the property will cost us less cash upfront, it’s also going to produce less cash flow after the debt service is paid each month.

- If you’re scared to death of debt or if you have a personal philosophy of avoiding debt at all costs – this approach will obviously conflict with that mindset.

The great thing about financing is that it has the potential to supercharge the growth of your real estate portfolio. When you can purchase properties quickly without tying up your own finite source of cash, you might be shocked at how quickly you can build up a MASSIVE source of wealth and incomefor years to come.

Deal or No Deal?

The bottom line is this…

If we purchase this property and pay all cash for it, we can reasonably expect to be $3,030 richer at the end of each year after taxes… and it will cost us $31,375.

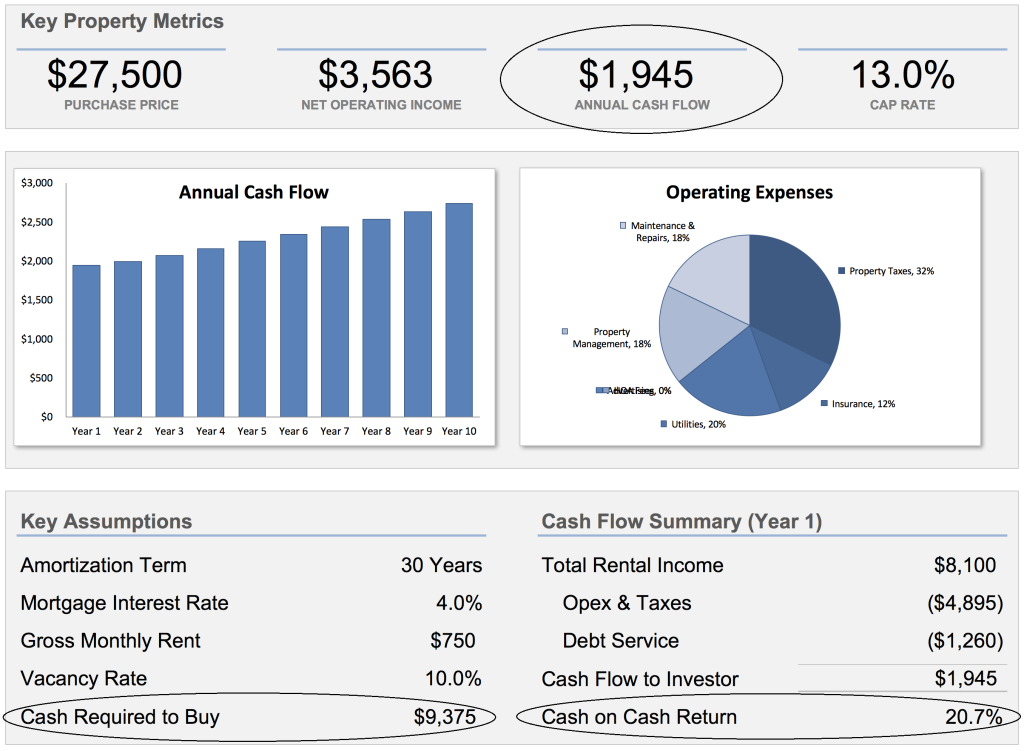

If we purchase this property with financing, assuming 20% down and 4.00% interest over 30 years, we can reasonably expect to be $1,945 richer at the end of each year after taxes… and it will cost us $9,375.

If you want a closer look at how I plugged all of these numbers into the PropertyREI calculator – I’ll walk you through the entire process in this video below…

Want to use the PropertyREI Rental Property Calculator?

You can get it at PropertyREI.com. And remember – be sure to use Promo Code: RETIPSTER1 at checkout for an instant 10% discount.

Making The Offer

When you know a deal makes sense on paper, it’s time to make an offer.

On December 15, I prepared a very simple, one page written offer for $27,500.

A couple of days after I emailed this offer to the seller – he called me and we spent some time haggling over the price on the phone. He obviously wanted as much as possible – but $27,500 was literally my ceiling (if the price went any higher, I wouldn’t have had a buyer on the other end – and I made this very clear to the seller).

On December 18 – I received the seller’s acceptance via fax.

The Necessity of Due Diligence

Whenever you’re making an offer – you have to make some assumptions.There’s no practical way around this.

It’s okay to assume some things (if your purchase agreement gives you the necessary wiggle room to get out of the deal) – but once your offer is accepted, you need to go through the motions of verifying that those assumptions wereactually correct.

As you conduct your due diligence, there will be almost always be some “findings” that come up in your research process (i.e. – things you weren’t aware of when you made your offer). The key is to know when these findings are acceptable and when these findings are a deal breaker.

Once we had this seller’s official “go ahead”, I ordered a home inspection report from a company called House Master (for a grand total of $385 – which my buyer agreed to reimburse me for). House Master is one of many home inspection companies that operates in my area.

There are a lot of home inspectors out there who do similar work… but if you happen to have a House Master in YOUR area, I can give you my official “thumbs up” recommendation. The team that handles my inspections does a great job – and the information they provide almost always results in me negotiating a lower price.

There are a lot of home inspectors out there who do similar work… but if you happen to have a House Master in YOUR area, I can give you my official “thumbs up” recommendation. The team that handles my inspections does a great job – and the information they provide almost always results in me negotiating a lower price.

While the inspector was there, I dropped in to do a quick visual inspection of my own.

I don’t always do this (in most cases, I can trust my inspector and property manager to give me an accurate assessment), but since I live just on the other side of town, I figured it would be prudent to swing by.

Here are a few pictures I snapped of the interior and exterior with my iphone:

As you can see – it was a pretty simple, small house. Not enough for anyone to retire off of, but not a bad property for a newbie investor to get their feet wet with.

A couple of days after the inspection, the folks at House Master emailed me their full, 51-page report, giving a VERY thorough overview of every observable issue that could come up with this property (honestly, it was more than I even wanted to know – and considering their job, this was a sign of a job well done).

Their report brought some pretty important issues to light – all things the seller didn’t tell me about, and things that would likely impact the cash flow of this property within the first couple of years after acquisition.

The most pressing issues were as follows:

- The furnace was still functional, but was near the end of its life (it was over 20 years old). Replacing it would definitely be a necessity in the near future, and it wouldn’t be cheap.

- The bathroom shower was leaking and needed some attention to fix the issue.

- The roof needed some patch work.

- Some of the siding had some holes in it and needed to be replaced.

- The kitchen faucet was leaking and the counter top had some chips in it.

Altogether, we figured these repairs would cost approximately $5,000 to fix.

Now obviously, I don’t expect any property to be 100% free of problems, but what I do expect is to understand what those problems are BEFORE anybody goes through with buying it (whether I’m buying it myself, or assigning the deal to another investor).

This was a tricky case, because I knew the seller had already come down quite a bit with his asking price, and he had no intention of going any further.

In most cases – I would keep pressing the seller to move further down (depending on their level of motivation), but rather than continuing to push this guy, I decided to adjust the “Deferred Maintenance Costs” in the PropertyREI calculator from $2,500 up to $5,000 to see what the deal would look like after accounting for these extra costs.

Cash Scenario:

Financing Scenario:

Fundamentally speaking, if this property was financed conventionally – it would still cash flow, it would simply reduce the cash on cash return from 20.7% to 16.4% and if the property was purchased with all cash, the cash on cash return would be reduced from 9.7% to 8.9%. The annual cash flow and net operating income would stay the same.

On both accounts, it was still a good deal… the numbers would just take a slight move in the wrong direction (though not enough to be a deal-killer). Given this, we decided to take the hit and move forward (something I don’t do often, but the deal was good enough that it warranted this kind of concession from our standpoint).

The benefit we had in this case was awareness. When these problems need to be addressed – we DON’T want to be surprised or “stabbed in the back” by the seller.

Closing Process

Once I knew our $27,500 was still acceptable after our property inspection, I emailed our fully executed purchase agreement to the title company and they began their title search on our behalf.

Once I knew our $27,500 was still acceptable after our property inspection, I emailed our fully executed purchase agreement to the title company and they began their title search on our behalf.

Now – when I’m REALLY pinching pennies, I do have the option of doing my own title search – but considering that my buyer was going to pay a significant amount of money for this property AND it involved an assignment of contract AND we needed someone to facilitate the signing of the closing documents, handing this job over to a title company was an easy decision.

With this particular property, my intent was to “assign the contract” to a third-party buyer.

In other words, my plan was to take my purchase agreement and sell the paper to another investor (a process that some refer to as “wholesaling”).

How Does Wholesaling Work?

When I signed this contract with this seller, they gave me the legal right to purchase this property for$27,500within a specified period of time.

Well – if for any reason, it’s not convenient for me to buy this property for $27,500 (e.g. – if I don’t have this kind of cash in my pocket at any given moment), but I know another investor who would LOVE to get this deal, I am literally allowed to sell this contract to them.

This is allowed because the seller gave me their written permission to do this (it is stated very clearly as an “assignment clause” in our contract).

This kind of transaction is completed with a 1-page form called an “Assignment Agreement”. This document is signed by ME (the “Assignor”) and the end buyer (the “Assignee”). The end buyer pays me a set amount of cash for the contract and in exchange, they can jump into my shoes and take my place as the Buyer in the original purchase agreement.

When Does Wholesaling Work Best?

This type of transaction tends to work best when a property is being purchased in an all-cash transaction (i.e. – the buyer doesn’t need a bank loan to purchase the property).

Why? Because whenever a bank gets involved with a real estate transaction, they have a tendency to add a lot of restrictions and rules that make it very difficult (if not impossible) for the wholesaler (i.e. – ME) to get paid.

Luckily, I was dealing with a cash buyer in this situation – which is part of what made the whole project possible.

The Assignment Fee

There are a couple of different ways that I charge assignment fees.

Method 1: If I have a property under contract for a ridiculously low price (say, 20% of market value) – I generally feel comfortable charging a sizable fee, simply because there is a HUGE profit margin available that I can pull from. If the deal makes sense, the seller will gladly pay it because even with the cost of my fee, they are still getting an awesome deal that they wouldn’t have found without my help.

Method 2: If I have a property under contract for a respectably low price (say, 50% of market value) – I will charge a 6% – 10% assignment fee (similar to a realtor commission).

Now to clarify… I am NOT a real estate agent (nor do I ever intend to become one). There is a distinct difference between what an agent does, and what I (as a wholesaler) do.

When I structure a deal like this, there is literally a purchase agreement signed between ME and the seller. Once this contract is signed, I have an marketable interest in the property.

A realtor doesn’t have this kind of arrangement. Instead, they are signing an agreement whereby the seller authorizes them to market the property on their behalf in exchange for a commission if/when the property sells.

Selling property on behalf of a property owner without a license isn’t legal. However, if you’re selling your marketable interest in the property (via your executed purchase agreement), this is a completely different scenario. This is a very important, key difference between these two types of business arrangements.

At The Closing Table

The closing process went very smoothly. The seller met at the office of our title agency in the morning, and my buyer met at the same office later that afternoon. During this process, the following things were transferred from the seller to my buyer:

- Current building inspection certificate

- Copy of the Current Tenant lease

- Tenant Unit Condition Checklist

- Original Tenant Application

- Tenant Security Deposit

- Keys to the House

My buyer then had to complete the following items with their new property manager:

- Execute a Management Agreement

- Execute a W-9 (IRS form)

- Sign Up for Direct Deposit (easiest way to get paid by their property manager)

- Hand Over the Keys to the House

- Hand Over the Security Deposit

The transaction was seamless and there were no major hiccups along the way.

What to Expect

During their first month of operations – my buyer earned a whopping $10 of rental income from this property (yippee).

There were a few reasons for the lackluster start:

- The tenant only paid $600 of their $750 rent to the previous owner

- There were some small, but immediate repairs that needed to be done

- The property management company had to recoup their initial start-up costs

This is the reality of owning rental properties. It would be very atypical for an investor to come blasting out of the gate with their best possible outcome on the first month. It just doesn’t work that way.

It’s not unusual for the first month of operations to be disappointing, but there are a few things to keep in mind.

- Often times, rental properties suck wind in the beginning. When you’re acquiring an older property with an existing tenant… be patient. Dealing with deadbeat tenants, repairing things that should have been fixed years ago, paying for sins of the previous property owner are ALL very real possibilities immediately after you buy. For this reason, ALWAYS be conservative when you’re creating your projections on a rental property. Not all sellers are “liars” – but as a general rule of thumb, don’t ever assume they’re telling you everything you need to know. I’ve dealt with a lot of reasonable, respectable sellers – but they still didn’t tell me 100% of the details. Allow some room for error when you’re evaluating the deal.

- Maintenance is something you’ll always have to save for. If you’re purchasing a property over 50 years old (which accounts for almost every property I look at), maintenance will be an even bigger issue to factor into your cash flow. This is okay IF you are buying the property for a low enough price. Just remember – when you buy an older property, you need to allow some room in your cash flow for some “question marks”. Be conservative and allow for some small, bad things to happen without putting you in the red.

- Build up a 6 month reserve and maintain it. You should always have a reserve of cash available to cover the costs of your property when it doesn’t cash flow. For example, if the tenant in this property decides to stop paying his rent altogether – he’s going to get evicted, no questions asked. If this happens, the property will be without revenue for at least 2 – 3 months, best case scenario (maybe even longer).

When I bought my first rental property, my property manager was very upfront with me and said:

“Plan for a net loss your first year.”

Even though I was getting a great deal and the projections looked awesome – he was still right.

When you’re dealing with some of the issues listed above, there are a lot of unknowns and things inevitably don’t go as planned. Be prepared for this.

A Look Back (One Year Later)

In this case study, we analyzed this property using the same process that has been proven by a lot of highly successful real estate investors. Our evaluation was thorough, we verified our assumptions and we took every feasible issue into account.

My buyer did end up having a lot of costs during their first year (judging by the age and known issues in the house) and they did eventually lose their tenant. However, in the months and years since, the rent price was adjusted upward to account for the stronger market for rentals that followed with the rebound of the real estate market.

Some of the known issues did take a toll on the property’s profitability during their first few months of ownership – but once the repairs were made and the right tenant was in place – they were able to consistently generate the monthly cash flow that was projected in our initial evaluation. They were also able to benefit from the additional tax write-offs that came with owning rental real estate like this.

Again – this is not (nor will it ever be) a property that throws off massive cash flow, but for someone’sfirst experience with a rental property, it’s an ideal way to get started in the business.

It generates some small supplemental income for the new owners and will be relatively easy to sell whenever they decide to liquidate the property (because this is a very generic, affordable property in a densely populated part of town). These are great attributes to have in a property when it comes time to sell.

Final Thoughts

As with any real estate investment – buying rental properties takes a lot of homework. Rental properties don’t necessarily come with the glamour and huge paychecks that “flipping houses” is known for – but it is a proven method of building multiple streams of permanent income.

If you’re looking to supplement your retirement income with something that comes with significant opportunities for appreciation, passive cash flow and tax benefits – buying properties (the right way) it a great way to make do it.

(The article was pulled from: http://retipster.com)